One of the best things you can do for your financial health is to learn how to audit your personal finances. This will help give you a roadmap for what changes and modifications you need to make, and help give you the action plan to make them.

What Is A Personal Finance Audit

An audit is an official inspection of an individual’s or organization’s accounts.

For this post, I’ll define a personal finance audit as a thorough review of your financial situation. It analyzes your income, expenses, debts, savings, investments, as well as other financial pieces.

I view a personal finance audit as a nitty-gritty budget review. I am evaluating every piece of my spending, culling what no longer benefits my financial goals, and reassessing my long-term financial view.

The end goal of auditing your personal finances is to identify areas where your financial health can be improved, aid you in making better spending decisions, and help you achieve your financial goals more effectively.

How To Audit Your Personal Finances

I’ll be honest, the process of auditing your personal finances can take some time. Whether you block out a day to get it done, or you do it slowly over a few weeks is totally up to you. But my suggestion is to complete the process until the end.

This process will help you understand where you are financially compared to where you want to be, and that is the first – and largest – step. Once you know where you are to where you want to go, defining the steps to get there will be much easier.

Gather All Your Financial Documents

This process will go much smoother if you have all your financial documents. This includes:

- Bank Statements

- Credit Card Statements

- Bills – Monthly & Non-Monthly

- Loan Statements

- Pay Stubs

- Receipts

- Tax Returns

- Insurance & Investment Account Statements

In order to keep this process streamlined, keep the statements to the last 3 to 6 months. For a more comprehensive audit, use documents from the past 12 months; this ensures that you’ve included any annual expenses that may have slipped through a shorter audit.

Organize your documents either chronologically, or by category to make them easier for you to review.

Review Your Income

The first step is to identify all the sources of income that you have. This includes salaries, bonuses, freelance work, rental incomes, interest from savings accounts, dividends, etc.

Make sure your income is accurately recorded; compare it to bank statements and/or paystubs to verify the amounts, and ensure consistency.

Track Your Spending

Once you’ve reviewed your income, the next step in a personal finance audit is to categorize your expenses for at least a month. This will help you see if there are any unnecessary expenses and any areas where you may be overspending.

When you list out all your expenses, divide them into categories such as fixed and variable expenses. Don’t be afraid to get nitty gritty with the categories. Lumping “coffee” or “books” into a “miscellaneous” category doesn’t help you see how much you are *actually* spending on coffee or books.

- Fixed expenses don’t change much from month-to-month, and don’t fluctuate much based on usage or consumption. These can also remain the same no matter the changes to your income and spending habits.

- Examples: rent/mortgage, streaming subscriptions, gym memberships, insurance premiums, car payments, loan payments, property taxes, and some utilities like internet and cell phone services, etc.

- Variable expenses fluctuate month-to-month based on your consumption, usage, or even discretionary spending habits. These changes can be tied to seasonal changes, unexpected needs, and varying lifestyle expenses.

- Examples: Groceries, transportation costs, clothing, entertainment, dining out, medical expenses, and some utilities like heating/cooling, water, and electricity.

As you complete this step, see if you can identify any patterns or trends within your spending. Are there some expenses that surprise you? What are some areas you could cut back on? Where would you need to allocate more funds?

By reviewing your income and your expenses as the first portion of your audit, you are ensuring that you’re not spending more than you earn. This is a vital step in your overall financial health.

You can head here to learn more about how to effectively track your expenses.

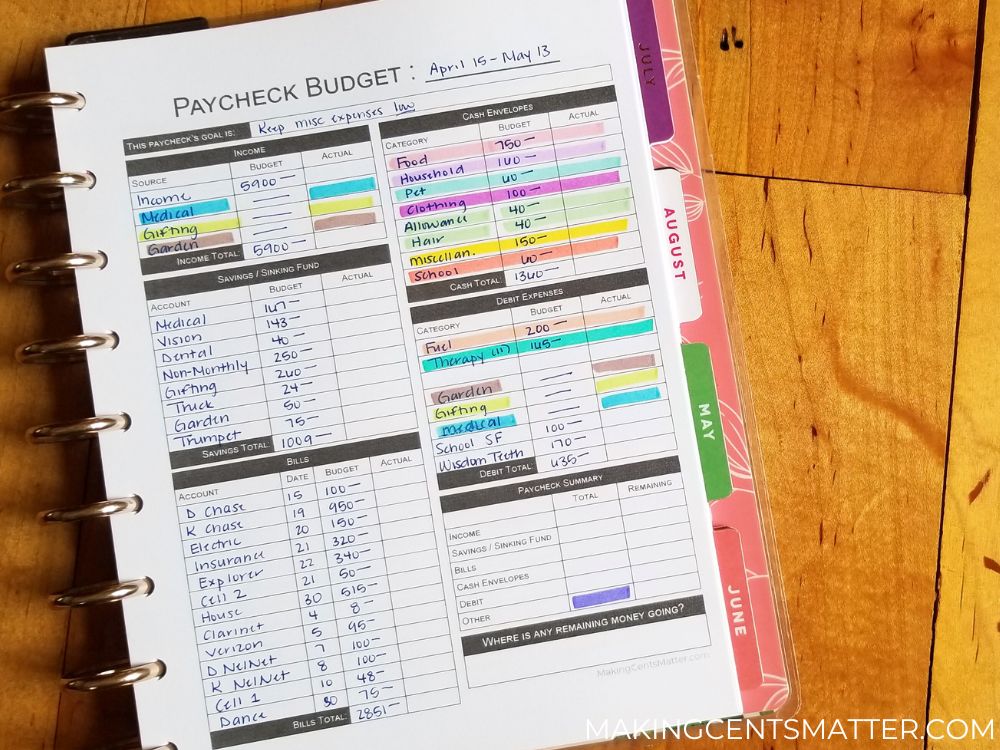

Compare Earnings & Expenses To Create A Budget

Now it’s time to compare your actual spending to your income, and create a budget!

Once you have a budget in place, it becomes easier to determine whether you are staying within your financial means. It can easily make adjustments to your budget when it’s necessary, such as with categories you are overspending or underspending in.

If you do not have a budget created, use your current income and expenses to create one based on your overall financial goals.

You can learn more about how to set up a Zero-Based budget here.

Review Your Debts & Liabilities

The next step in a personal finance audit is to list out all outstanding debts you have, noting the interest rates, minimum payments, and total balances for each debt. These can include:

- credit card balances

- student loans

- car loans

- mortgages

- personal loans

Also note any terms of each loan, such as penalties for early payment.

In order to pay off your debts, prioritize them based on either interest rates or balances. Paying off by smallest to largest balance (debt snowball) will give you boosts in motivation as you pay off your debts, while prioritizing by interest rate from highest to lowest (debt avalanche) will help save money in the long run.

Consider any options for debt consolidation or refinancing; if it can reduce your interest rates and monthly payments.

Remember, there is no “one size fits all” when paying off your debt. Whichever route you choose, make at least minimum payments on all other debts while you focus on paying off your prioritized debt account.

Evaluate Your Investments & Savings

After you evaluate your debts and liabilities, it’s time to look at your assets. To know where your financial health stands, you need to know what assets you have, and how they compare to your liabilities.

Examine your savings accounts, checking accounts, retirement accounts, and any investment portfolios you have. Are they currently meeting your expectations, or do you need to modify them to align with your financial goals?

Carefully consider whether you should rebalance any investments you have to ensure that you are taking full advantage of any retirement offers you have available to you, such as employer match retirement.

Need to learn how to start saving for an emergency fund? Start saving in these 8 simple steps.

Review Your Credit Report

Reviewing your credit report as a part of a personal finance audit will allow you to know whether your credit score needs improving, or if any inaccuracies need to be disputed. If your goal is to own a house, you’ll want to ensure you have a good credit score for interest rates and loan terms to be advantageous.

You can get a free credit report annually from the three major credit bureaus.

Create (or adjust) Your Financial Goals

If you haven’t made any financial goals yet, now is the time to make them!

Looking through your personal finances audit, what stood out to you as spending habits you want to break, or savings goals you wish you had achieved by now? Use these to define your short-term and long-term financial goals.

Once your goals are defined, break them down into smaller, manageable, and actionable steps – that are bound to a timeline – to help you achieve your goals.

You can read this article to learn more about how to create financial goals, and how to define them using the S.M.A.R.T. method.

Monitor Your Progress

The final step to learning how to audit your personal finances is to implement the changes, and monitor your progress!

Whether you implement the changes as a habit tracker to track days you spend less or no money or set up automatic transfers for savings and investment accounts, these changes will help you make the necessary adjustments that are needed to reach your overall financial goals.

What Are The Benefits Of Auditing Your Personal Finances

- Refined Budget Discipline: learning how to audit your personal finances leads to improved financial discipline, ultimately helping you control your spending.

- Greater Financial Clarity: completing a financial audit gives you a better understanding of where your money is going, and how you can manage it effectively. This also leads to easier financial decisions.

- Realistic Goal Setting: creating and establishing realistic personal finance goals, along with the plan necessary to achieve them.

- Better Debt Management: reinforcing positive financial habits that help you to create a plan to pay off your debts more efficiently. You have the potential to save money on interest payments as you are paying off your debt.

- Optimizing Savings Opportunities: by identifying areas you can save more money, and invest wisely, you can improve your investment and saving strategies.

- Improved Credit Score: knowing how to audit your finances will help you maintain, and improve, your credit score by identifying, then addressing, any issues. The earlier you catch any disputes, the easier it will be to resolve them.

Have you audited your personal finances lately? What is one change you regularly make, or one step that you find helpful after your audit? Let me know in the comments below!

Leave a Reply