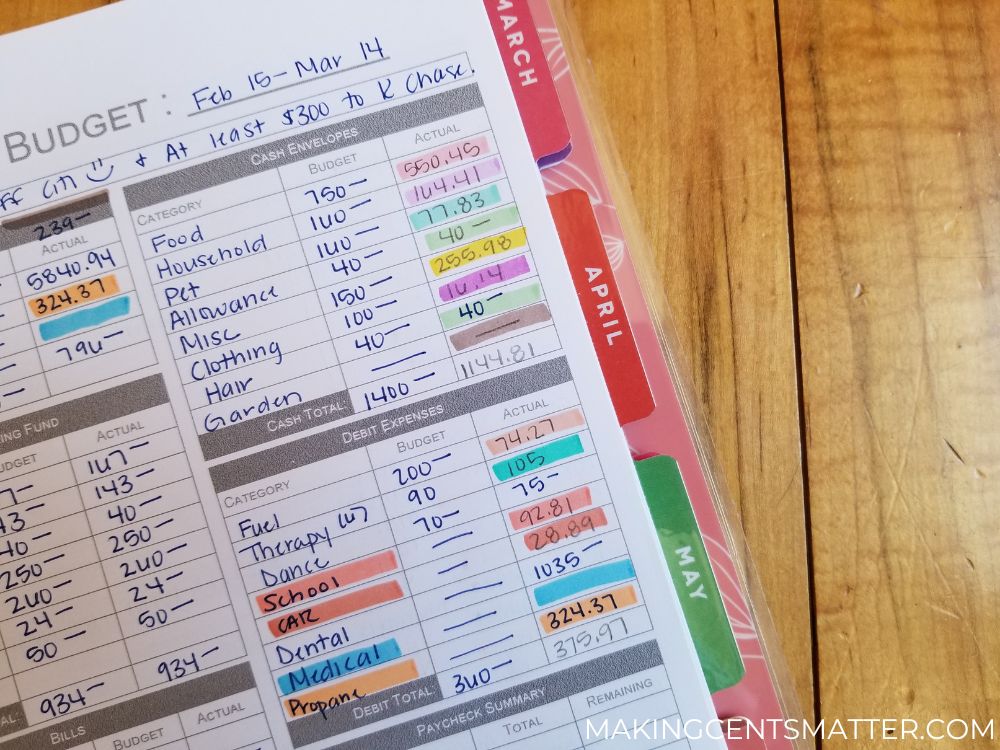

Creating a zero-based budget is one of the easiest ways to begin budgeting, and take control of your finances. The beauty of this type of budget is that it ensures that every dollar has a designated purpose. Here is a step-by-step guide for how to create a zero-based budget.

Note: This is a reformatted version of a previous post. Please READ THIS if you’d like more information.

Before we get into how to create a zero-based budget, I want to point out the definition of a budget. It is something that I refer to a lot.

A budget is an estimation of income and expenses for a set period of time.

An estimation. Remember that things change from week to week, month to month, and year to year. A budget needs to change based on your priorities at that time.

Related Posts:

- How To Create A Percentage Budget

- 8 Steps To Creating Your Emergency Fund

- How A Budget Calendar Helps You Budget Effectively

- Brilliant Budgeting Goals For Beginners

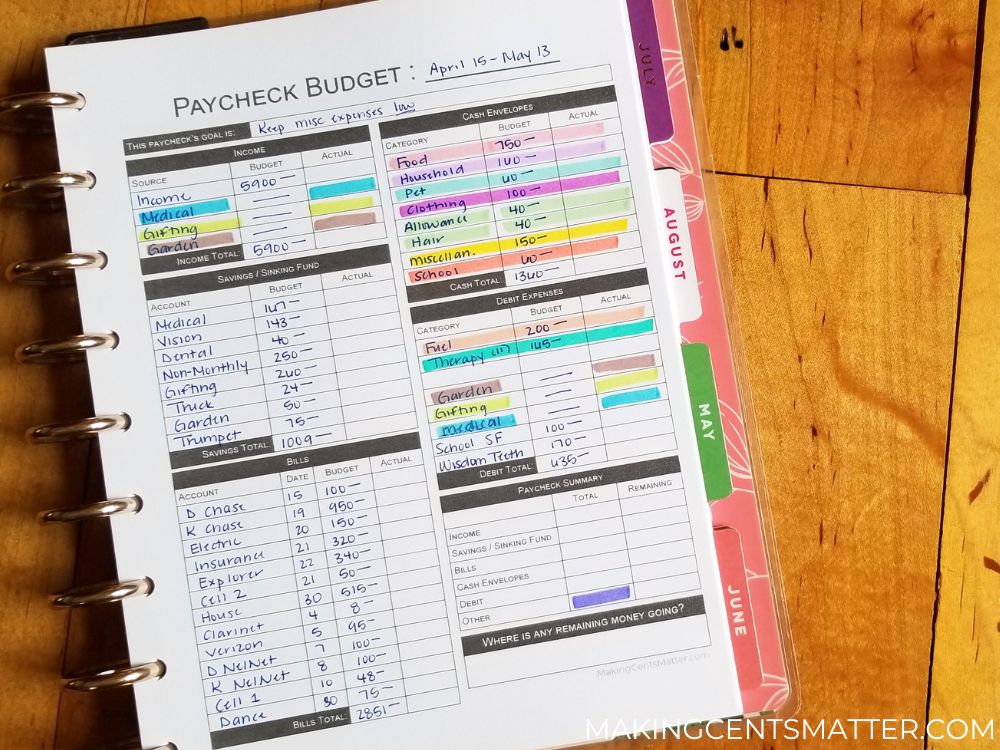

Calculate your Total Income

Gather all the sources of income that you have within a specific time period. The most common period is monthly, but a zero-based budget will work with any time frame once you get accustomed to it.

Be sure to include any regular income, as well as any income you receive from passive streams, side gigs, and freelance income. The total of all sources is what is used as a starting point for your income.

List Out Your Estimated Expenses

Look at your calendar for the period you’re using, and list out all the expenses you’ll have.

Categorize the expenses into fixed and variable.

- Fixed expenses don’t change much from month-to-month, and don’t fluctuate much based on usage or consumption. These can also remain the same no matter the changes to your income and spending habits.

- Examples: rent/mortgage, streaming subscriptions, gym memberships, insurance premiums, car payments, property taxes, and some utilities like internet and cell phone services, etc.

- Variable expenses fluctuate month-to-month based on your consumption, usage, or even discretionary spending habits. These changes can be tied to seasonal changes, unexpected needs, and varying lifestyle expenses.

- Examples: Groceries, transportation costs, clothing, entertainment, dining out, medical expenses, and some utilities like heating/cooling, water, and electricity.

Understanding the difference between fixed and variable expenses within your own budget will help you be able to plan and allocate your funds more effectively. Apply these guides to make informed decisions on your own budget.

Make Sure That Every Dollar Has A Job

Assigning every dollar a job is how this budgeting style got its name! You want to zero out your budget. As you are evaluating your current financial goals and aligning your budget to meet those priorities, you may want to rearrange how you give every dollar a job. That is okay!

Here is a good place to start with your zero-Based Budget:

- Begin with the essential expenses, like housing, utilities, debt, and transportation costs.

- Next, prioritize any savings goals you are working towards.

- Then allocate funds towards groceries, clothing, pet costs, etc.

- Lastly, any remaining funds can be used towards increasing your monthly debt payment, adding to your savings goals for the month, and any discretionary spending you have.

Prioritize Your Expenses; Adjust Where Necessary

Remember to start with the most crucial expenses. This helps to make sure that you’ve covered the necessities before allocating any money towards discretionary spending.

If your income isn’t covering all your expenses, you need to prioritize your expenses, make adjustments, and cut back spending where you can. An alternative, if the season of life you are in allows, is to find an additional source of income.

Track Your Spending

By consistently tracking your expenses throughout the month, you can help make sure you are sticking to your budget. You can track your expenses through budgeting apps, spreadsheets, or manually.

I prefer to track my expenses on paper since there is a link between writing things down and being more connected with what you are writing.

You can learn more about how I track my expenses here.

As you become accustomed to budgeting, you can adjust your categories as you need to if you find you are overspending in one, and underspending in another.

Have You Created A Zero-Based Budget Before? You Can Find My Free Zero-Based Budget Printable In My Resource Library, and Check Out My YouTube Channel For Examples Of How I Set Up A Zero-Based Budget On A Monthly Income.

Leave a Reply