Whether you are new to budgeting or have been managing your finances for a while, there is one tool that will help you achieve your financial goals. Using a calendar for budgeting is a practical way to gain control over your expenses by visually breaking down your budget. This allows you to plan, track, and manage your finances throughout the month. Here’s a step-by-step guide on how to use a budget calendar to manage your finances effectively.

Note: This is a reformatted version of a previous post. Please READ THIS if you’d like more information.

What is a Budget Calendar?

In its simplest terms, a budget calendar is a calendar that is used to track your budget.

A budget calendar structures your budget so that you can plan your household finances, visualize your income and expenses, track progress on your financial goals, and make financial decisions that work toward your financial goals.

While you can use a digital calendar or a spreadsheet as a budget calendar, this post focuses on using a paper budget calendar.

While you could add all your financial obligations to your main calendar, I like having a monthly calendar specific to my budget. I already know that when my calendar gets too full, I avoid what is on it and go into autopilot mode. Inevitably, this means things get left behind. However, having a calendar specific to my finances means that I can then transfer the necessary reminders for my budget to my main planner.

Related Posts:

- Brilliant Budgeting Goals For Beginners

- How To Complete A Budget Review – and Why You Should!

- Your Complete Guild To A Cash Budget

How can a budget calendar benefit me?

The concept of a budget calendar didn’t make much sense to me initially. I was always stuck visualizing my budget as a set calendar month. But rarely are people paid on the first of the month. Most paydays fall on Thursdays, every other Friday, or the 15th of the month.

I was trying to fit our Zero Based Budget to the traditional calendar constraint, and it simply wasn’t working. When we would have a payday on the 4th of the month, and our mortgage was due on the 1st, I couldn’t use a traditional calendar for our budget.

It wasn’t until I read You Need A Budget* that it clicked; I needed to use my current money for my current financial obligations. Not the money that was coming throughout the month.

How to create & use a budget calendar:

Creating a budget calendar is very simple.

What you’ll need:

- Calendar – the calendar shown in this post is printable of mine, but you can use whatever calendar you want.

- Pen or Pencil

- Highlighters – I like the bold colors of the Stabilo Highlighters*, but if you’re looking for something more reasonably priced, these Sharpie Highlighters* are an excellent substitute.

- White-Out

- Your schedule

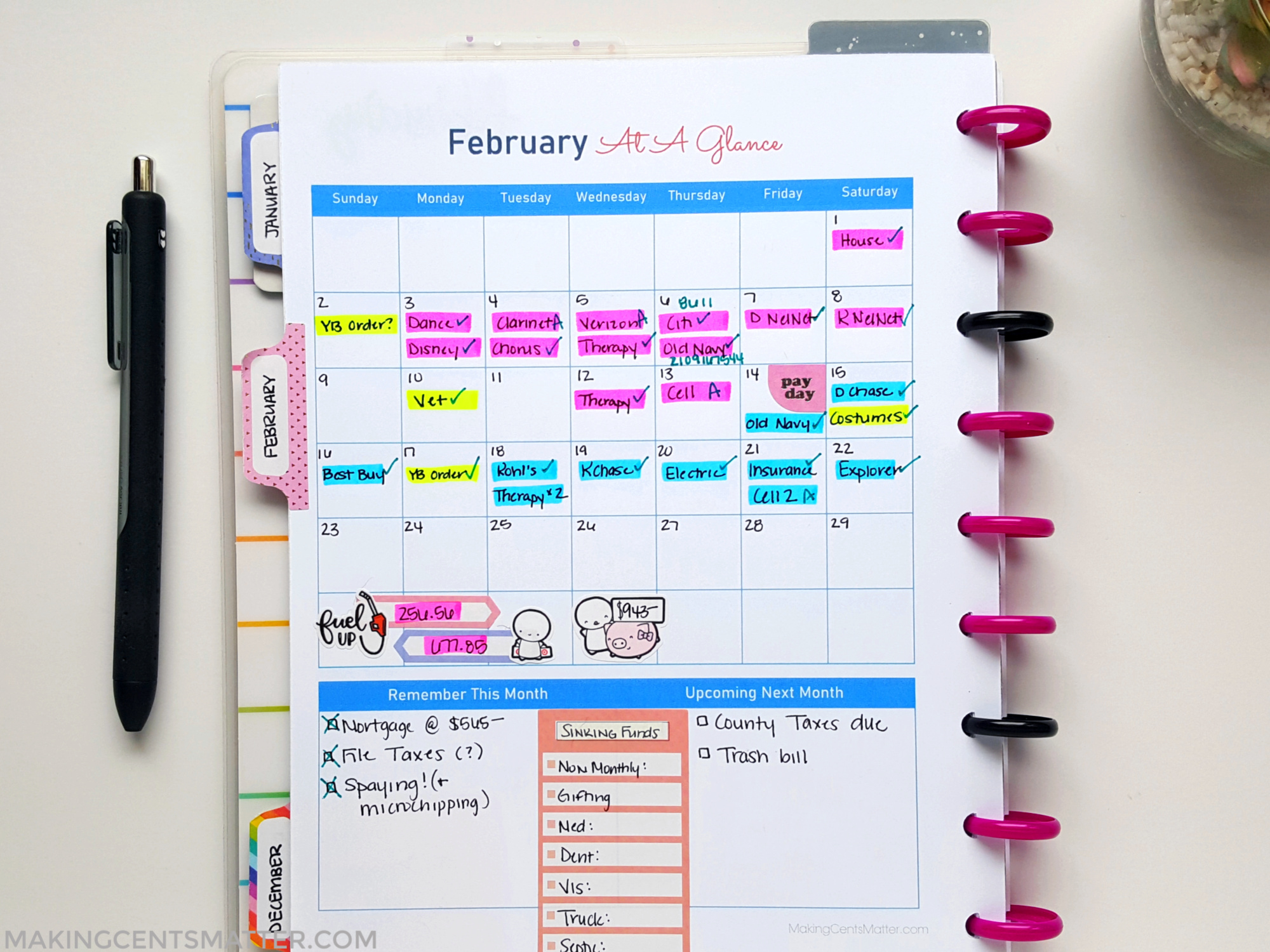

Whether you use a desk calendar, a separate insert in your planner, or my printable budget calendar bundle, the important thing is that you have a calendar.

To Set Up Your Budget Calendar:

- Mark your pay dates with different highlighter colors. This helps you see how your paydays are spread apart.

- Mark any due dates for bills, loan payments, subscription due dates, and other financial commitments, using the same color coding for their corresponding payday.

- Reference your personal calendar to mark any upcoming school events, sporting events, birthdays, holidays, and other anticipated financial expenses that occur during that month.

- Reference this calendar as you set up your paycheck budgets, remembering to prioritize your financial obligations.

As the month goes on, you will need to make adjustments. This is normal! Review how your budget meets your financial needs, then plan to meet your future financial needs.

Remember to remain consistent as well. Set up reminders and alerts for regular reviews, and don’t forget to utilize reminders and alerts for consistency. Regularly update your budget calendar so it will remain accurate to your financial priorities; this allows adjustments to be made easily based on your habits and goals.

What are the benefits of using a budget calendar?

There are a few benefits of using a budget calendar. One of the biggest benefits of using a budget calendar is that it takes your financial obligations and goals, and puts them in a visual timeline.

Visualizing your finances:

Your budget calendar should provide you with a clear representation of all your financial obligations, but focus on your income and your planned expenses (such as bills, utilities, etc.)

The visual aid helps you see at a glance what your cash flow is, making it easier to make informed decisions, remain accountable towards your financial objectives, and manage your finances effectively.

A budget calendar takes your financial obligations and goals, and puts them in a visual timeline.

Increase Budget Awareness

By using a budget calendar, you have a better awareness of your spending habits and financial responsibilities. This encourages you to be mindful of where the money is going and helps empower you to make better-informed decisions about your personal finances.

Better Organization:

Utilizing a budget calendar, and color-coding, aids in organizational skills by structuring your finances within set time frames, reducing the amount of missed payments and overspending.

When I organize my finances on a calendar, I easily learn my spending patterns. This helps me to see that when one paycheck has more bills than another, I can either schedule the bills ahead of time to a paycheck that doesn’t have as many bills or minimize my variable expenses during that week by meal planning, meal prepping, and grocery shopping in preparation the week before.

Reduce Financial Stress and Anxiety:

When you have a visual of your budget over the month, you can be proactive about your expenses, due dates, and timelines. Knowing what upcoming expenses are planned and accounted for helps reduce financial-related stress and anxiety since you are effectively budgeting and managing your money.

You can even take your budget calendar one step further, and create a Year-At-A-Glance. This helps you to see what expenses that are not monthly are coming up, enabling you to allocate funds towards those essential payments effectively.

Aids in Financial Decision-Making:

Using a budget calendar allows you to make well-informed decisions that are aligned with your short-term and long-term financial goals. It helps you see when there are opportunities to save more or cut back on spending.

Learning how to use a budget calendar helps to serve as a practical, visual tool for your financial organization and accountability, empowers you to achieve your financial goals, and be more informed of your financial decisions.

Leave a Reply