Do you often feel like there is always more month than money? If so, you are not alone! Many people – including even me! – struggle from time to time with effectively managing their finances. It isn’t a good feeling when you wonder where all your money has gone. One of the best ways to take back control over your financial situation is to conduct a spending analysis.

What Is A Spending Analysis?

A spending analysis is when you honestly and systematically review every financial transaction you have made over a specific period. Completing a personal spending analysis helps you categorize and evaluate your expenses. The reason this is important is that it allows you to identify trends and areas where you can make strategic improvements for your overall financial health.

Spending Analysis vs Tracking Expenses

Just looking at a glance, conducting a personal spending analysis seems like it’s the same as tracking your expenses. But in reality, it’s not. They each serve a different purpose in your finances and can supplement each other.

When you are tracking your expenses, it involves recording every dollar that you spend, and how it lines up with the budget estimate you set. The overarching goal for tracking expenses is to document all your spending. This helps to ensure there are no spending leaks. You can also easily see where you are under- or overestimating expense categories within your budget.

However, a spending analysis goes even deeper. It’s like a financial snapshot, but just for your spending rather than your overall finances. The analysis helps you categorize and evaluate your spending patterns, such as hidden fees. It also helps you identify where your spending isn’t aligning with your financial goals.

In short, tracking expenses is about recording your budget, while a spending analysis is about understanding your habits and optimizing them for your goals.

Spending Patterns That An Analysis Can Uncover

You’d be amazed at some of the insidious spending we do that can impact your overall financial health. Below is just a small example of spending patterns that an analysis can uncover:

- Frequent & Recurring Small Expenses – At the time, frequently made small purchases don’t seem like much (coffee, candy bars, etc), but they can add up to a large sum over time.

- Seasonal Spending Trends – While this expense is obvious for heating and cooling, other seasonal expenses increase only during specific months. Gardening, back-to-school, vacations, and holidays can highlight times when adjustments to your budget are needed. These expenses can easily have sinking funds created for them.

- Forgotten Subscriptions – Free trials can quickly become paid services that we forget about and are continually charged for.

- Emotional Spending Triggers – Emotions affect our finances more than we know! Are you noticing you are spending more when you are stressed, bored, or even celebrating a birthday or holiday?

- High Fees & Interest Charges – ATM charges, credit card interest payments, and even recurring overdraft fees can be costing you much more than expected.

- Inconsistent Savings Contributions – Nothing is worse than believing you have the money in savings, only to realize you have been contributing sporadically to your savings account.

- Planned vs Impulse Purchases – Tracking your spending patterns can help reveal whether larger purchases are being efficiently planned out or are frequently made as an impulse.

- Gap In Cash Flow – Those times where money seems to run out before you are paid again can indicate an uneven management in your cash flow. An analysis can help you see that you need to adjust your spending and saving patterns.

- Groceries vs Eating Out – There are seasons where eating out happens more frequently than others. By making sure you are accounting for those changes in your spending, you’re not overspending on groceries just to end up eating out.

- Lifestyle Creep – Many people find that as their income rises, their discretionary spending amounts rise as well. In the end, this habit prevents long-term savings growth, and can affect your overall financial health.

Why You Need To Complete A Spending Analysis

This particular financial tool is incredible in helping you analyze where you are spending your money, identify any wasteful spending habits you have, and help you to create a plan for improvements within your finances. Here are 5 ways that completing a spending analysis helps to improve your overall finances.

1 – Identifies Problem Areas

By pinpointing specific areas where you are overspending, you can create a plan to tackle the individual issue. Your plan to tackle unused subscriptions is much different than your plan to decrease your impulse purchases.

2 – Encourages Better Budgeting

By understanding your specific spending habits, you can easily create a realistic budget that is aligned with your financial goals.

3 – Reduces Financial Stress

Gaining some clarity on where your money is going helps to reduce any anxiety you feel about your finances and gives you the feeling of control over your personal finances.

4 – Increases Savings Potential

After identifying non-essential expenses, you can redirect those funds toward savings, investments, or even debt repayment.

5 – Improves Financial Decision-Making

With a clear view of your spending, you can make better financial decisions when it comes to cutting costs that are unnecessary to your budget or even effectively allocating funds for your financial goals.

What Are The Pros and Cons of Conducting A Spending Analysis?

As with any strategy to help improve your overall financial health, creating a spending analysis has its pros and cons.

Pros:

- Increases awareness of exactly where your money is going

- Identifying problem areas to help you prevent overspending, allowing you to stay within budget

- Effortless financial goal setting that is in alignment with your current financial circumstances

- Encourages financial planning by pointing out where funds need to be allocated to reach your goals

- Grows your savings and accelerates your debt repayment by freeing up extra money

- Improves accountability and intention within your finances by understanding your financial habits

Cons:

- Time-consuming to review your transactions and categorize expenses, especially when done manually

- Requires consistency to make sure you are making progress in reducing unnecessary expenses, and changing spending habits

- Can reveal some hard truths about your finances, making it difficult to brainstorm potential changes

Despite these few challenges, the benefits – especially in the long term – of completing a spending analysis far outweigh any drawbacks. Think of it as a worthwhile investment in the future of your financial health.

How To Create An Effective Personal Spending Analysis

Ready to take the deep dive and analyze your spending? Here are the steps you’ll need to take to complete your personal spending analysis.

1 – Gather Your Financial Data

Before you can look at your spending, you’ll need all the statements of your spending over the last 3 to 6 months. The more data you have, the more accurate your analysis will be. However, if this is your first time conducting a spending analysis, I recommend looking at no more than expenses over the last three months.

Places where you can find your expenses include your expense tracker, receipts, financial statements, bank account transactions, and credit card records.

Use caution when using statements from the bank or credit card. Their statements can categorize your spending based on location.

If you stopped at the gas station to fill up but also grabbed a snack and a drink inside, both transactions will appear on your statement as “automotive”. The same goes for when you shop at a Target or Walmart; those transactions can appear as “uncategorized” on your bank statements, even though you purchased pet, clothing, baby, and food supplies.

2 – Categorize Your Expenses

Break down your expenses into different categories, such as:

- Fixed Expenses – rent/mortgage, insurance, loan payments

- Variable Expenses – groceries, eating out, entertainment, miscellaneous shopping

- Savings & Investments – sinking funds, emergency funds, retirement contributions

- Debt Payments – credit cards, student loans, personal loans

The more detailed you can get about your expenses, the better your analysis will be.

3 – Identify Spending Patterns

This is where a detailed spending analysis will become helpful. It’s time to look for trends within your spending and to get brutally honest with yourself. By answering the following questions, you can get started taking a deep dive into identifying spending patterns.

- What are my top three spending categories each month?

- Do I spend more on certain days of the week?

- How much of my spending is essential vs discretionary?

- What are some categories that I can cut back on?

- What automatic payments or subscriptions are no longer needed?

- Have any recurring expenses increased without my knowledge?

- What emotional triggers cause me to spend impulsively?

- Do my spending habits align with my short-term and long-term goals?

4 – Compare Your Expenses To Your Income

Compare your total monthly expenses to your monthly income. Are you living within your means, or are you spending more than you earn?

If your expenses are greater than your income, adjustments within your spending are necessary.

5 – Set Short-Term Financial Goals

Using what you learned above, set some realistic financial goals. Whether it’s starting a sinking fund, increasing your emergency fund contribution, or taking your debt repayment strategy into overdrive, use what you have learned and make changes that can work for you.

To make the goals realistic, there needs to be a gradual change. You cannot expect to cut off a habit of buying coffee every morning to jump-start a sinking fund. You can expect to reduce the number of days you buy coffee each week until you have created a new habit.

6 – Create An Action Plan

Based on your findings and the short-term financial goals you set, it is time to create your action plan.

For example, if you do buy coffee every morning but have a goal of reducing it to two days a week within a month, your action plan would look like:

- First week: Buy coffee 5 days this week, make coffee at home 2 days

- Second week: Purchase coffee 4 days this week, make at home 3 days.

- Third week: Buy coffee 3 days this week, make at home 4 days

- Fourth Week: Buy coffee 2 days this week, make at home the other 5

Don’t forget you need to plan ahead to make your action plan productive. If you usually buy coffee on in-service days, make sure the weeks with in-service days count toward your buying coffee days. This helps you adhere to your action plan and gives you more motivation to stick to your goal.

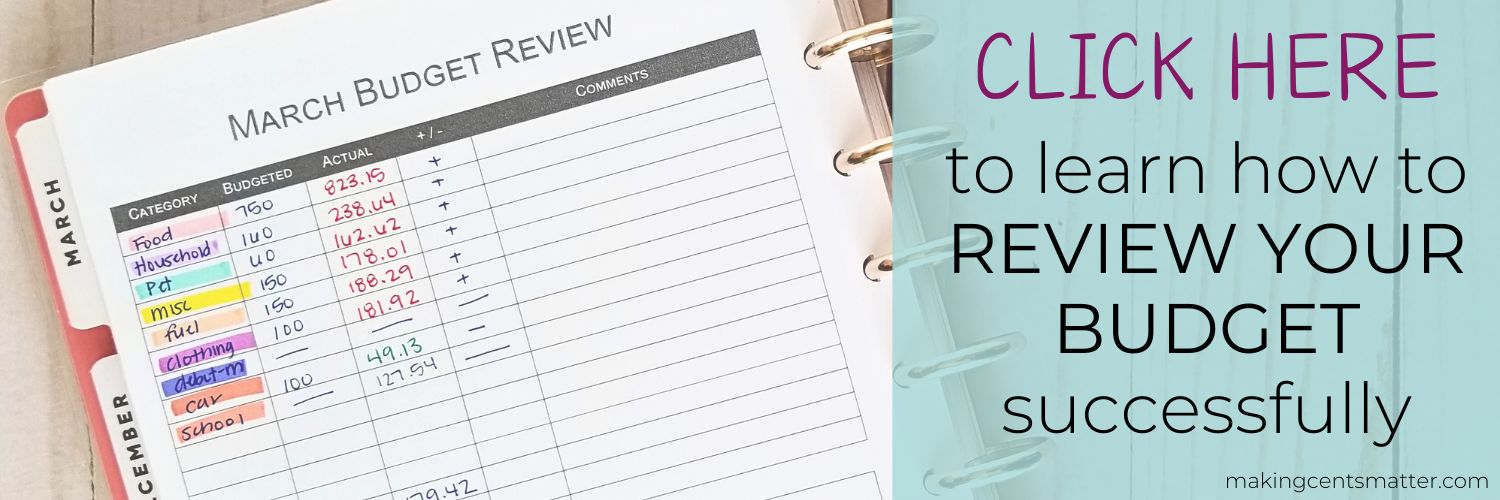

7 – Review Regularly And Adjust As Needed

Remember that your spending analysis isn’t a one-time task. You need to regularly review your spending. If you are already tracking your expenses diligently every month, analyzing your spending once a quarter won’t be as tedious. Since you are technically tracking your progress as you go (within your expense tracking), adjusting your spending to meet your goals will become far easier.

Final Reflection:

Analyzing your spending can be initially time-consuming and reveal some hard truths about your spending patterns, but the insight you will gain will lead you to smarter financial decisions, increased savings, and reduced financial stress.

Leave a Reply